Portfolio Overlay Strategies

This is a Paragraph Font

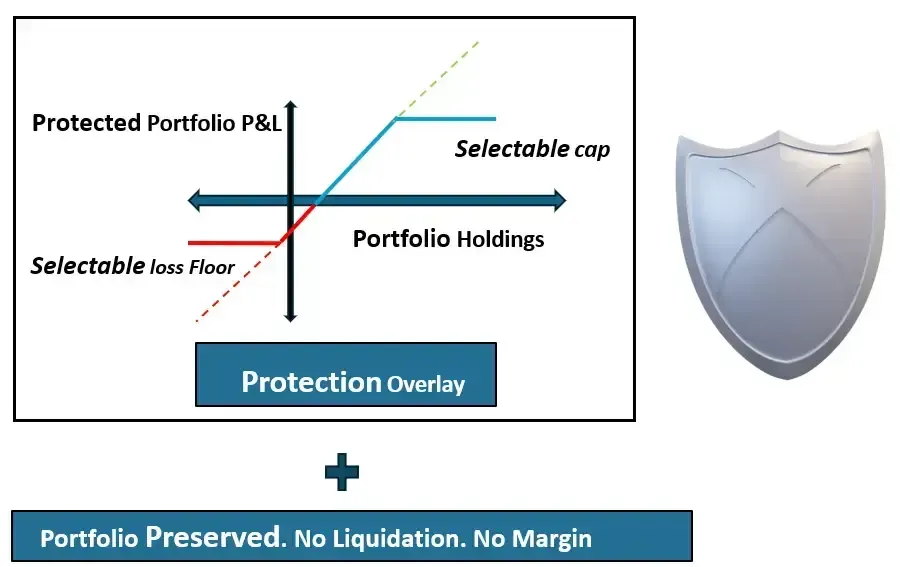

HEDG Overlay Strategy

Protect and Preserve

HEDG

Protection of Existing Portfolio as per Risk Tolerance.

This overlay strategy utilizes mostly Zero or Low-Cost-Collars defining the performance of the Portfolio at the end of protection period. Strategy also attempts to manage the portfolio so that underlying Portfolio Positions are not called away. For positions which don't have liquid Option Chains, an Index proxy is used. Collars are actively monitored.

The Floor-Cap and duration of Portfolio Protection are selectable.

HEDG strategy creates "SWAN IN BLACK SWAN" effect. Sleep-well-at-night during Black Swan events or periods.

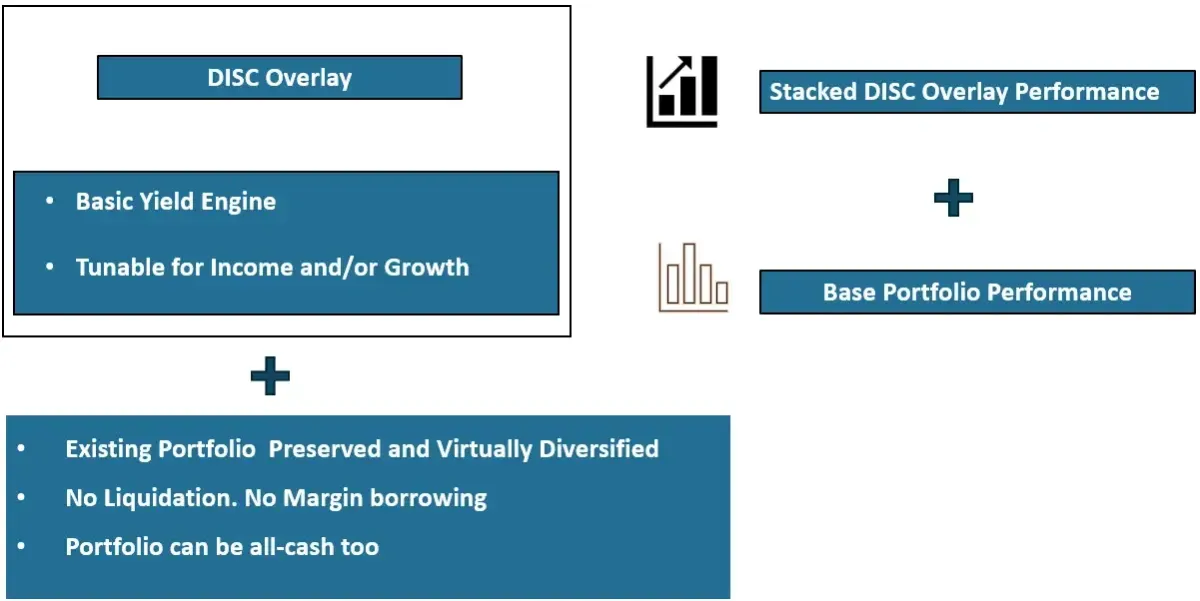

Tunable Yield Engine

DISC

This strategy is the main yield generation engine deployed on the Portfolio. It attempts to harvest the difference between yield of Dividend paying Stocks/ETFs and the prevailing Interest rates. The strategy recognizes that Dividends are reflected in the pricing of Call and Put options. It also bounds the risk to known level.

Note that the Portfolio Positions are not liquidated, nor does it use any conventional high-cost margin borrowing. Parameters for yield generation are fully selectable targeting Income or Growth. Yield engine performance is independent of the base Portfolio performance. Stacked performance is achieved in this strategy.

DISC Overlay Strategy

(Dividend Interest Rates Spread Capture)

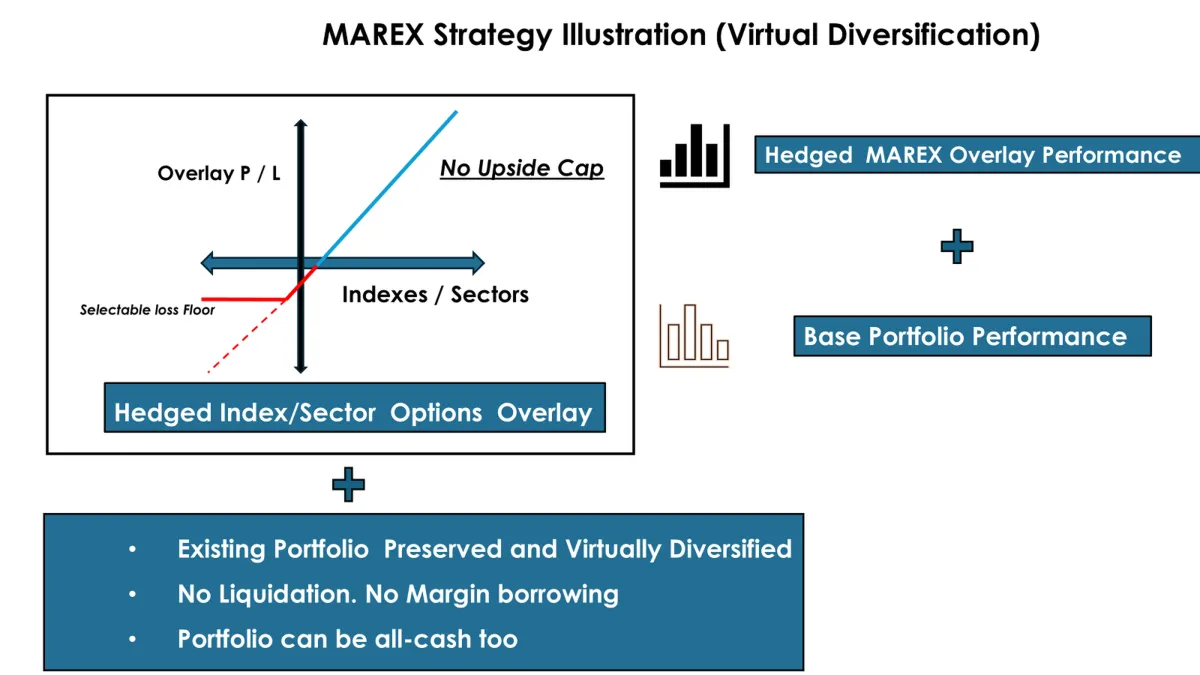

MAREX Overlay Strategy

(Market Exposure. Virtual Diversification)

MAREX

This strategy achieves Broad Market Exposure to (SPX, NDX, DJX, RUT) or any other market sector without portfolio liquidation. It "virtually diversifies" portfolio positions and creates a hedged exposure to broad market or sectors.

Note that the Portfolio Positions are not liquidated, nor does it use any conventional high-cost margin borrowing. Broad market exposure positions enjoy IRS 1256 code benefits (gains/losses are 60% Long Term and 40% Short Term).

This strategy also addresses concentrated positions problem. Stacked performance is achieved in this strategy.

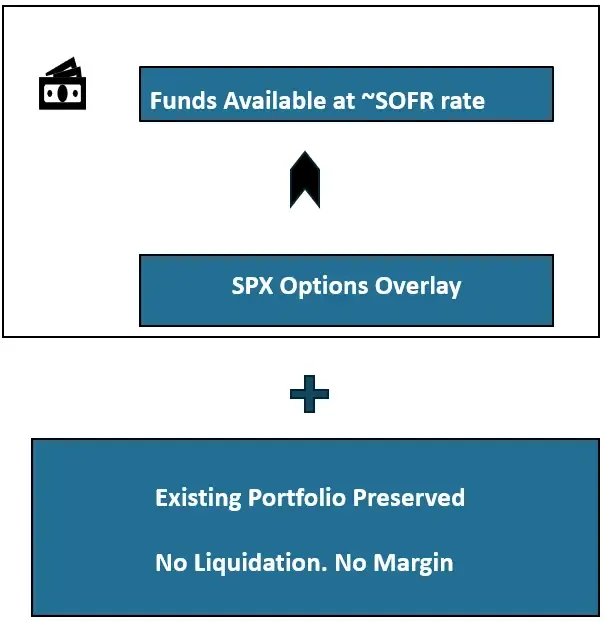

Low-cost cash borrow

POCASH

This strategy allows low cost cash borrow against the securities held in the Portfolio. The borrowing rate is close to the prevailing SOFR rate. Conventional margin or Securities Based Lending rates are much higher than SOFR. This strategy saves on Interest cost

Principal and Interest are payable only at the end of the term. Interest accrues at approximately SOFR rate.

The interest "cost" is treated as capital loss. Borrowed funds can be repaid any time without penalty.

Soman Advisors will refinance if interest rates come down.

POCASH Overlay Strategy

Disclaimer and important information

The strategies listed are for Illustration and Education purposes only

There is no explicit or implicit guarantee of future performance of these strategies

All investments involve risk of loss of Principal

These strategies rely on Options instruments which are derivative products and have their own risks

Contact Soman Advisors for further discussion of these strategies

Soman Advisors, LLC is a California-registered investment adviser. Information is for educational purposes only and does not constitute investment advice.

All investments involve risk, including loss of principal. Options and derivatives strategies involve additional risks and may not be suitable for all investors.

COMPANY

COMPANY

CONTACT US

CONTACT US

CONTACT US

Copyright 2026. Soman Advisors. All Rights Reserved.